By Justin Esarey

Last week, I assigned an exam problem for my graduate methods class wherein they would re-examine the Reinhardt-Rogoff result linking decreased GDP growth to increased national debt. They examined this hypothesis in the Quality of Government data set, a product of scholars at the University of Gothenberg that aggregates many separate databases into one large file. The key variables come from the UN World Development Indicators between 1991 and 2011. These variables are:

- wdi_gdpgr: GDP growth as a % of previous GDP

- wdi_gdpcgr: per-capita GDP growth as a % of previous per-capita GDP

- lag_wdi_cgd: the prior year’s central government debt as a % of GDP

We use last year’s debt to predict this year’s growth in an attempt to force the causal arrow to go from debt to growth, rather than from growth to debt. If Reinhardt and Rogoff are correct, then last year’s central government debt should be a good predictor of this year’s total and per-capita GDP growth.

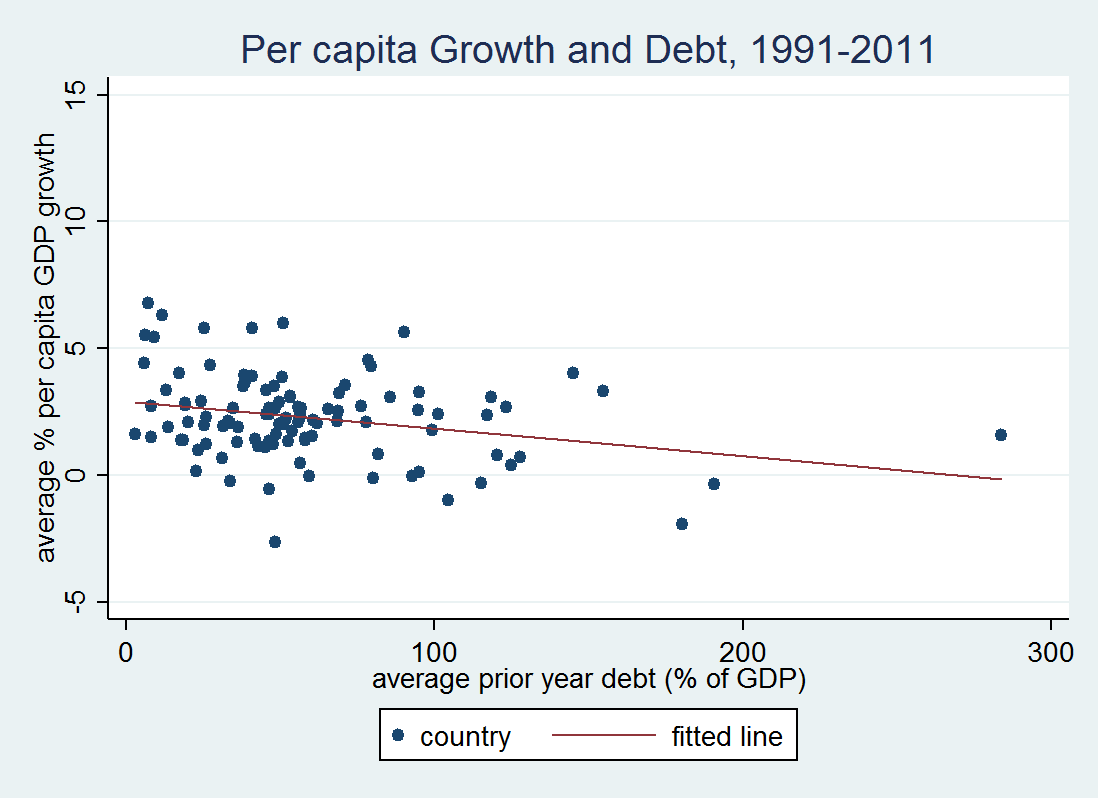

Start off by looking at the basic link between average prior year’s debt to average current year’s GDP growth, where the averaging happens over all observations in the time span. As the scatterplot below shows, there is a slight negative relationship: every 10 percentage point increase in debt is associated with a -.06123 percentage point decline in GDP growth. Hence, going from no debt to 100% of GDP in debt is associated with 6/10ths of a percent of a decline in growth. That effect is miniscule.

A somewhat stronger result holds when we look at debt’s relationship to per capita GDP growth. In this case, every 10 percentage point increase in average debt is associated with a -.108 percentage point decline in GDP growth. This is large enough to be noticeable (the relationship is statistically significant, p=0.004 two-tailed in a bivariate regression): a country with debt equal to 100% of its GDP would have 1% lower per capita growth compared to a country with no debt.

These conclusions are borne out if we look at a more complicated, multivariate model that tries to control for the impacts of unit heterogeneity, inertia in growth rates, and sources of spurious correlation. The most comprehensive model I tried was a mixed-effects panel model allowing unit heterogeneity (on the intercepts) by country, and using a country-level predictor of averaged debt as well as year-by-year debt to differentiate the impact of instant changes in debt vs. carrying a persistently higher debt load in the long run.

The results for the GDP growth model are shown below. This model adds many variables to the baseline model:

- lag_wdi_gdpgr: last year’s GDP growth, to account for potential inertia in growth rates and to recognize the fact that prior year performance might influence how much debt is accumulated (presenting a source of spurious correlation)

- lag_wdi_gdpc: last year’s per capita GDP level in constant US dollars, to block pathways from country wealth to growth and debt

- lag_wdi_puhe: last year’s public expenditures on health care as a % of GDP, to account for a potential source of spending that could be correlated with both debt and growth

- lag_wdi_ge: last year’s total government expenditures as a % of GDP, to account for overall government size as a potential cause of debt and growth

- lag_wdi_fr: last year’s fertility rate, to block influences on population growth as a mechanism of action for any of the variables above

- avg_debt: the country-averaged debt levels over the time period of the study

The results show, perhaps unsurprisingly, that average debt and last year’s debt have counteracting relationships with GDP growth. When debt is accumulated, it has a small, positive association with next year’s growth (that we cannot distinguish from zero effect in this sample). This is reflective of the idea that countries tend to have lower growth rates when they accumulate debt. But high levels of average debt are negatively associated with GDP growth. Countries carrying an average of 100% of their GDP as debt would experience 2.5% less growth in any given year compared to countries carrying 0% of their GDP as debt.

We see the same basic dynamics at work in examining per capita GDP growth; the table below shows my results. Again, increasing debt has a positive association with growth in the next year, with every 10 percentage points increase in debt associated with about 0.1 percentage points more per capita growth. Average debt levels over the entire time span are associated with less growth: countries that carry an average of 100% of GDP in debt experience 3.2 percentage points lower per capita GDP growth compared to states with 0% of GDP in debt.

However, all of these effects are dwarfed by an apparent strong, negative relationship between public spending on health care and GDP growth in this sample! Every 1 percentage point increase in public health expenditures (as a % of GDP) is associated with 0.38 percentage points lower GDP growth and 0.23 percentage points lower per-capita GDP growth. The models block potential spurious associations of health expenditures with fertility rates, with overall social wealth, or with government expenditures as a whole. Yet still, there are apparently very large and in my mind extremely curious relationships here.

I really can’t make sense of this, either theoretically or as some kind of error in my data or analysis. And I definitely don’t think that this conclusion is sound enough to become a part of the political conversation! A note to any reporters reading this: I do not think that more public spending on health care lowers growth! But I do think that the relationship, which I’ve plotted below, is interesting enough to warrant further investigation.

My data and analysis code are available here.